U.S. Corporation Income Tax Return

Legally Tax Saving · Local CPA Team · Filing Across All 50 States · Professional & Efficient

Our Service

Corporate Income Tax

Corporate tax is levied on a U.S. company’s annual net profit.C-Corporations must pay federal corporate income tax and possibly state corporate taxes.For LLCs, profits are passed through to the members or shareholders, and the entity itself does not pay federal corporate income tax.Federal tax rate: A flat rate of 21% applies.

Payroll Tax

Payroll tax refers to the federal and state taxes that employers must pay when compensating employees. It primarily funds Social Security and Medicare programs.Employers are required to withhold and remit the employee’s portion and pay their own share on time.

Failure to file and pay payroll taxes properly may result in significant penalties.

Sales Tax

Sales tax is a consumption tax collected by businesses from end consumers when selling goods or certain services, and then remitted to state or local governments.Key features: The federal government does not impose sales tax. Tax rates are set independently by states and local jurisdictions, typically ranging from 4% to 10%.

Self-Employment Tax

this tax is the Social Security and Medicare tax paid by individuals who work for themselves,without an employer.It is equivalent to both the employee and employer portions of payroll tax combined.This tax applies to:Sole proprietors;Independent contractors / freelancers;Members of an LLC

State Income Tax

State income tax is imposed by individual state governments based on a company’s or individual’s income, state of registration, or place of operation.Tax rates, calculation methods, and filing requirements vary widely by state.Some states, such as Nevada, Florida, and Texas, have no state income tax at all.

Franchise Tax

Franchise tax is a fee charged by certain states on businesses for the privilege of being registered or operating in that state, regardless of whether the business is actively generating income.It is not based on company profits, but rather on the company’s existence or authorized status.Even if a company has no operations or earnings, it must still pay franchise tax as long as it is legally registered.

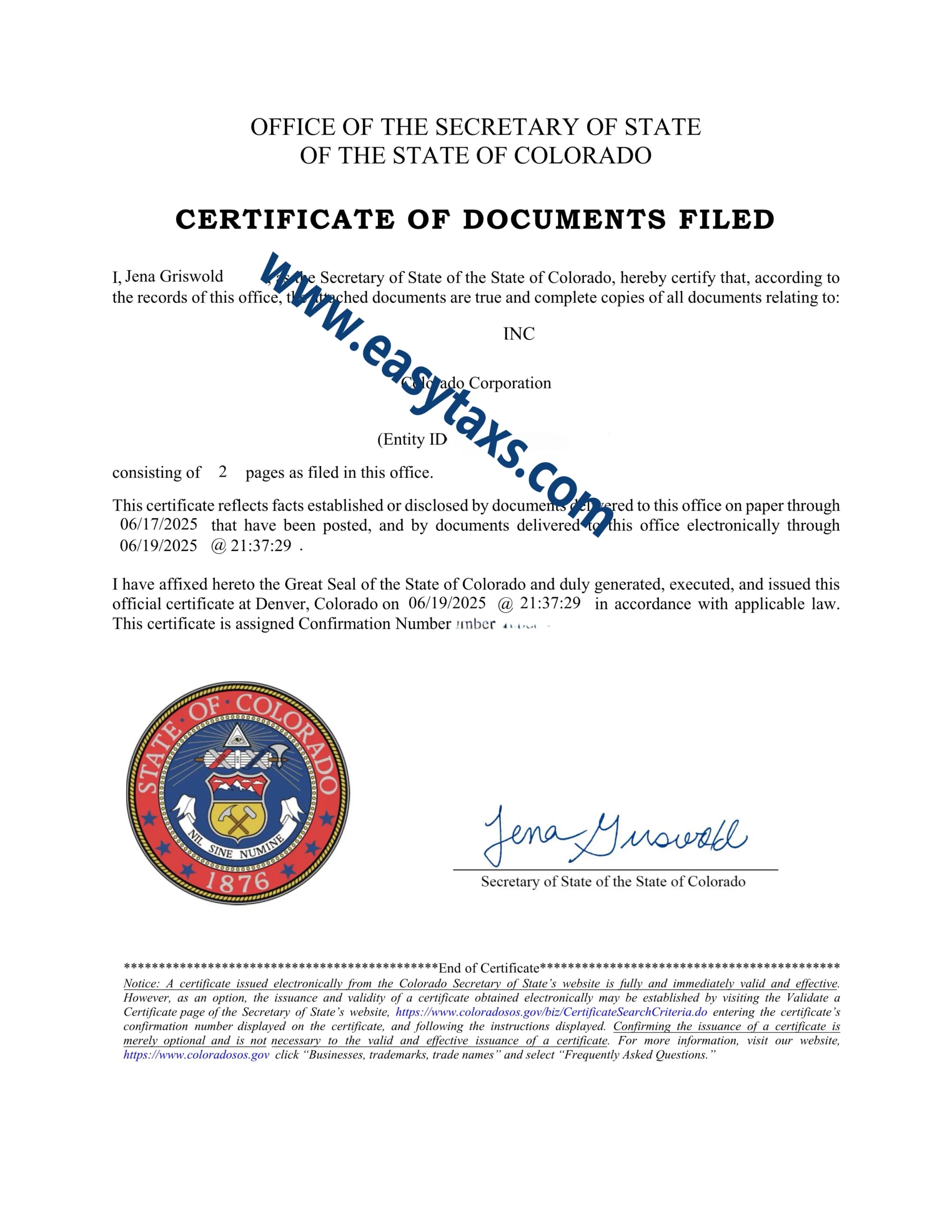

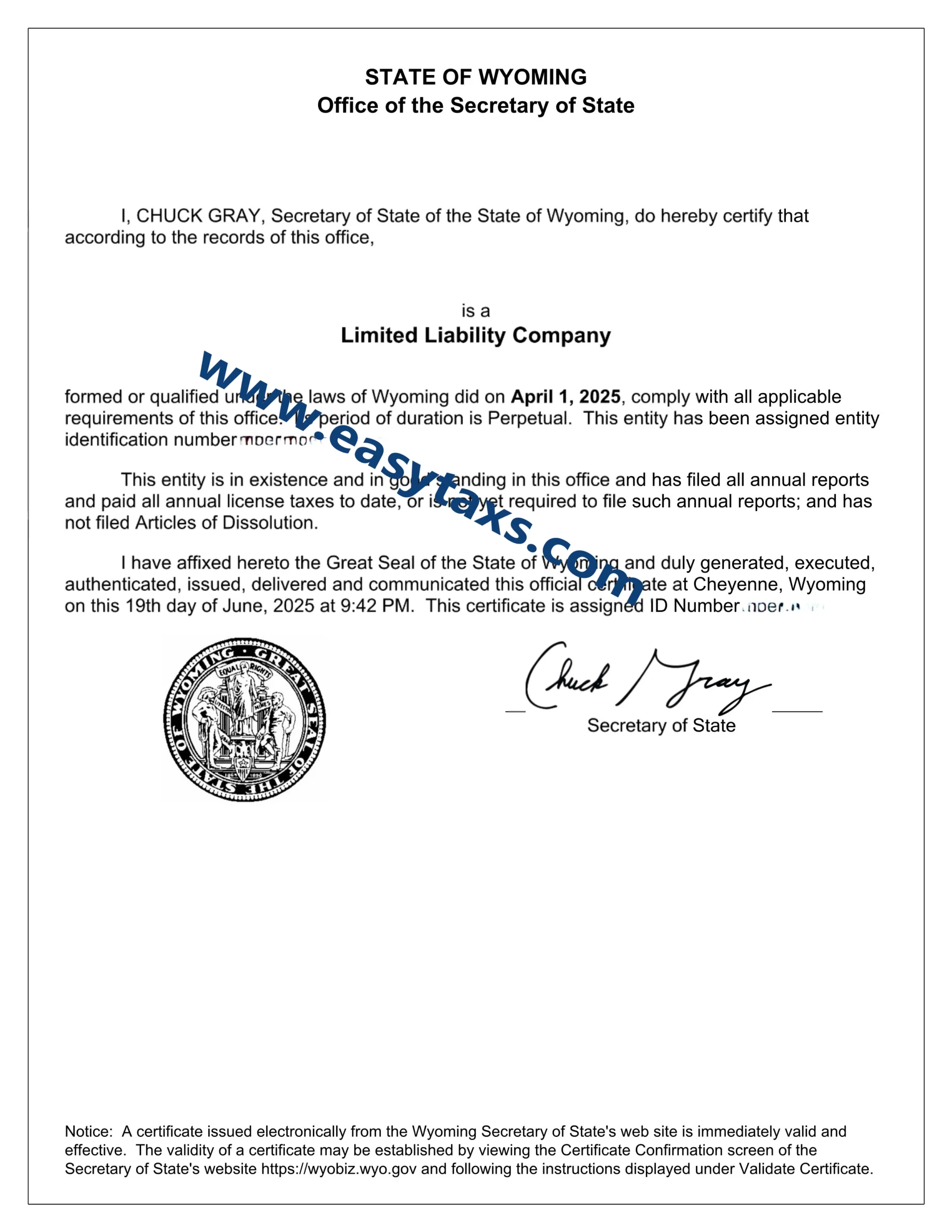

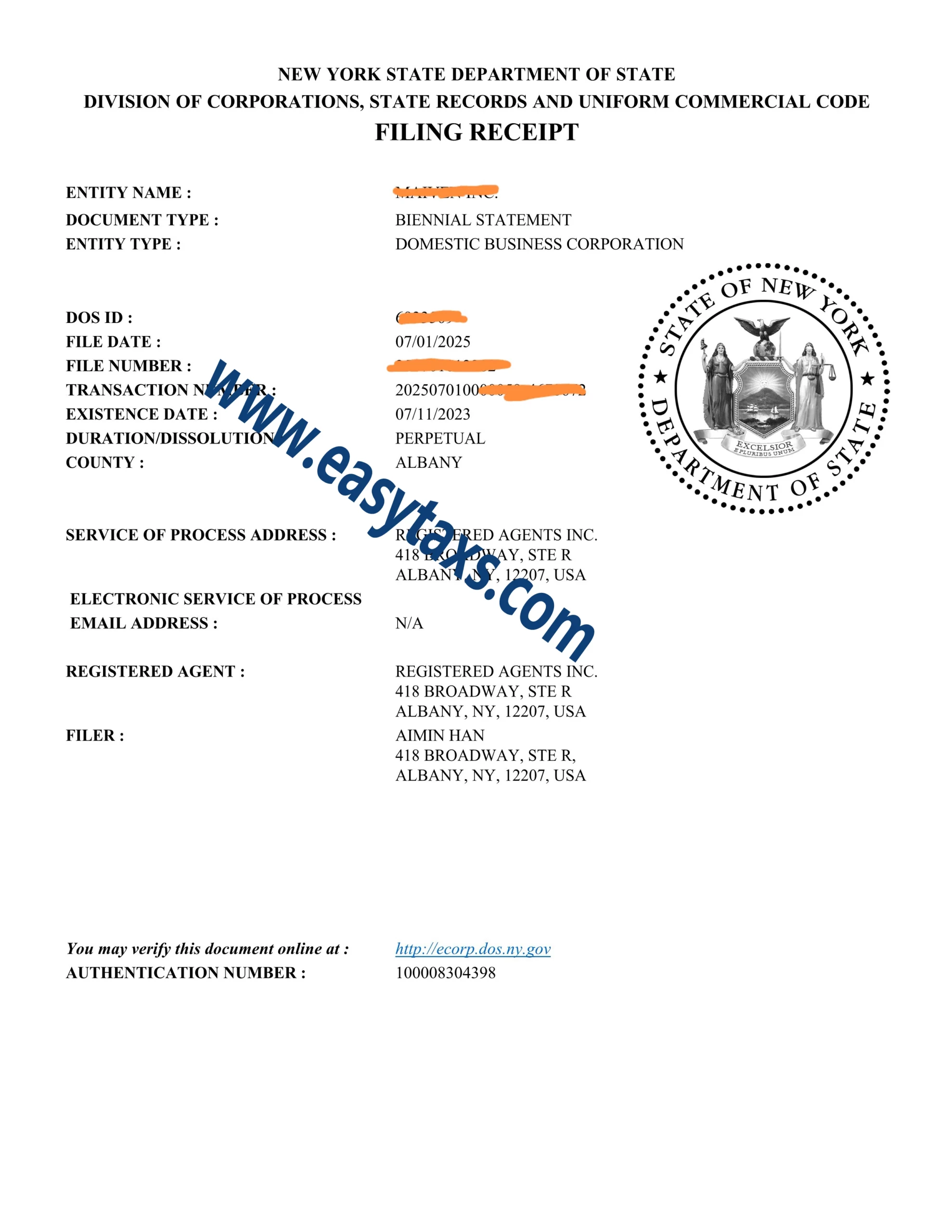

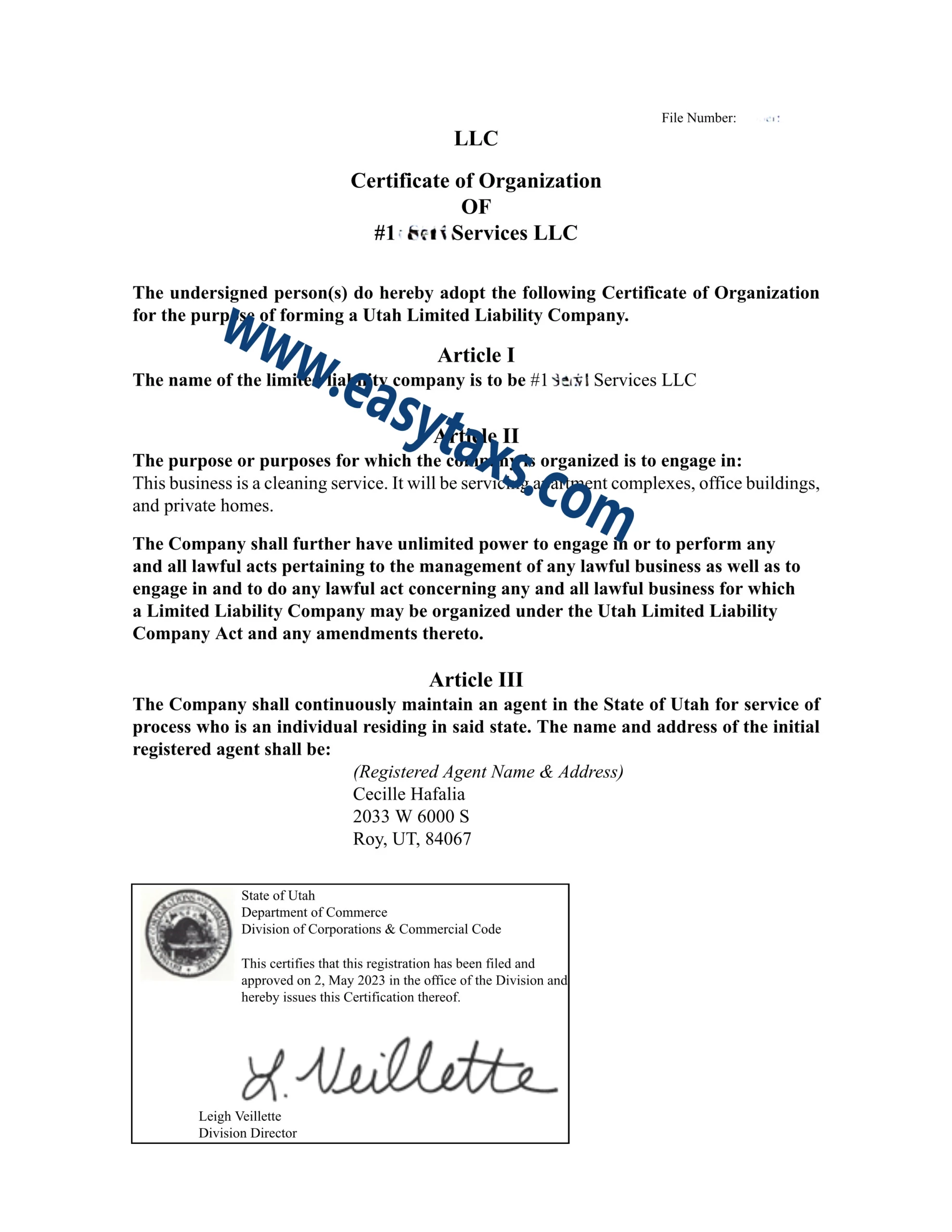

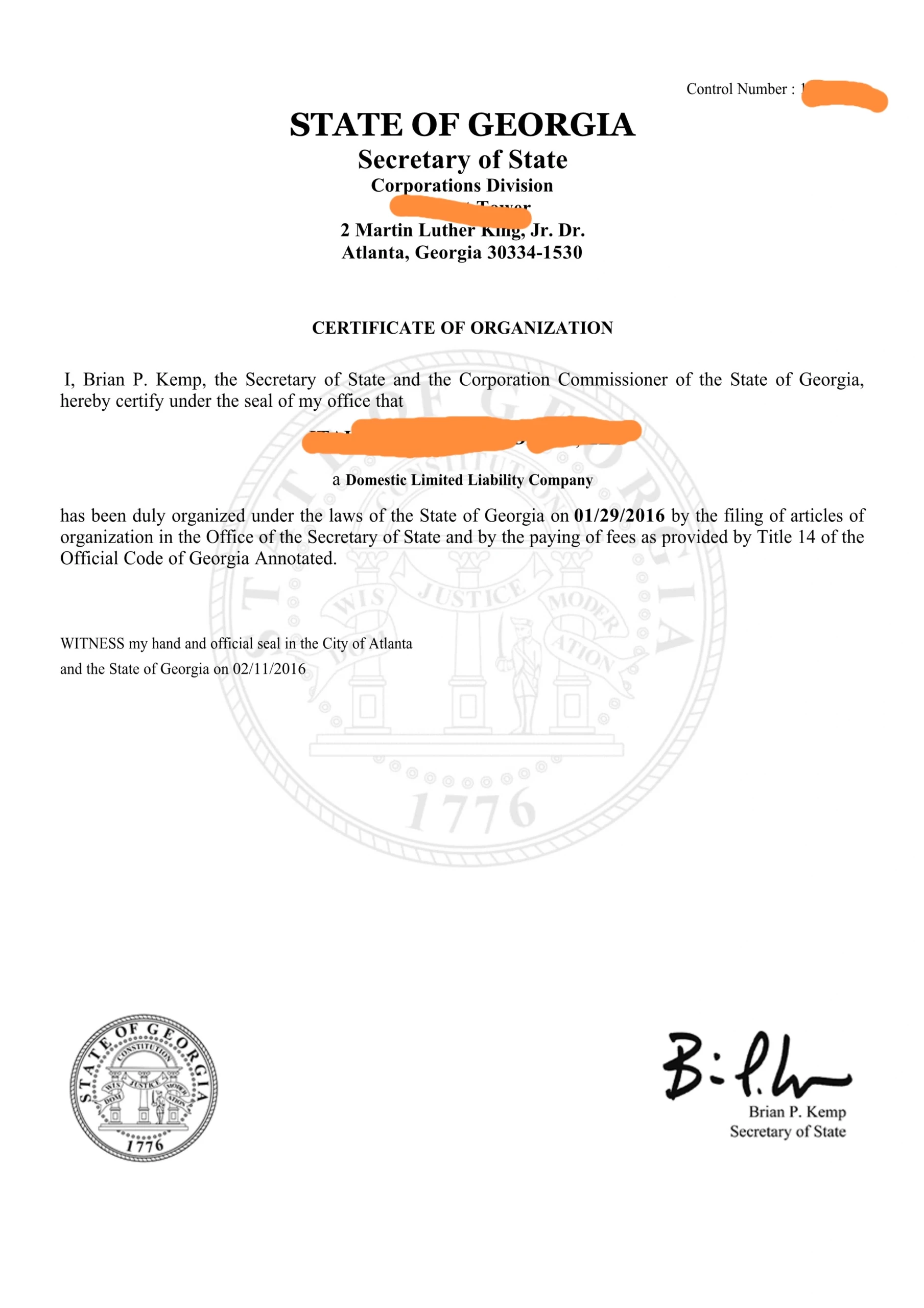

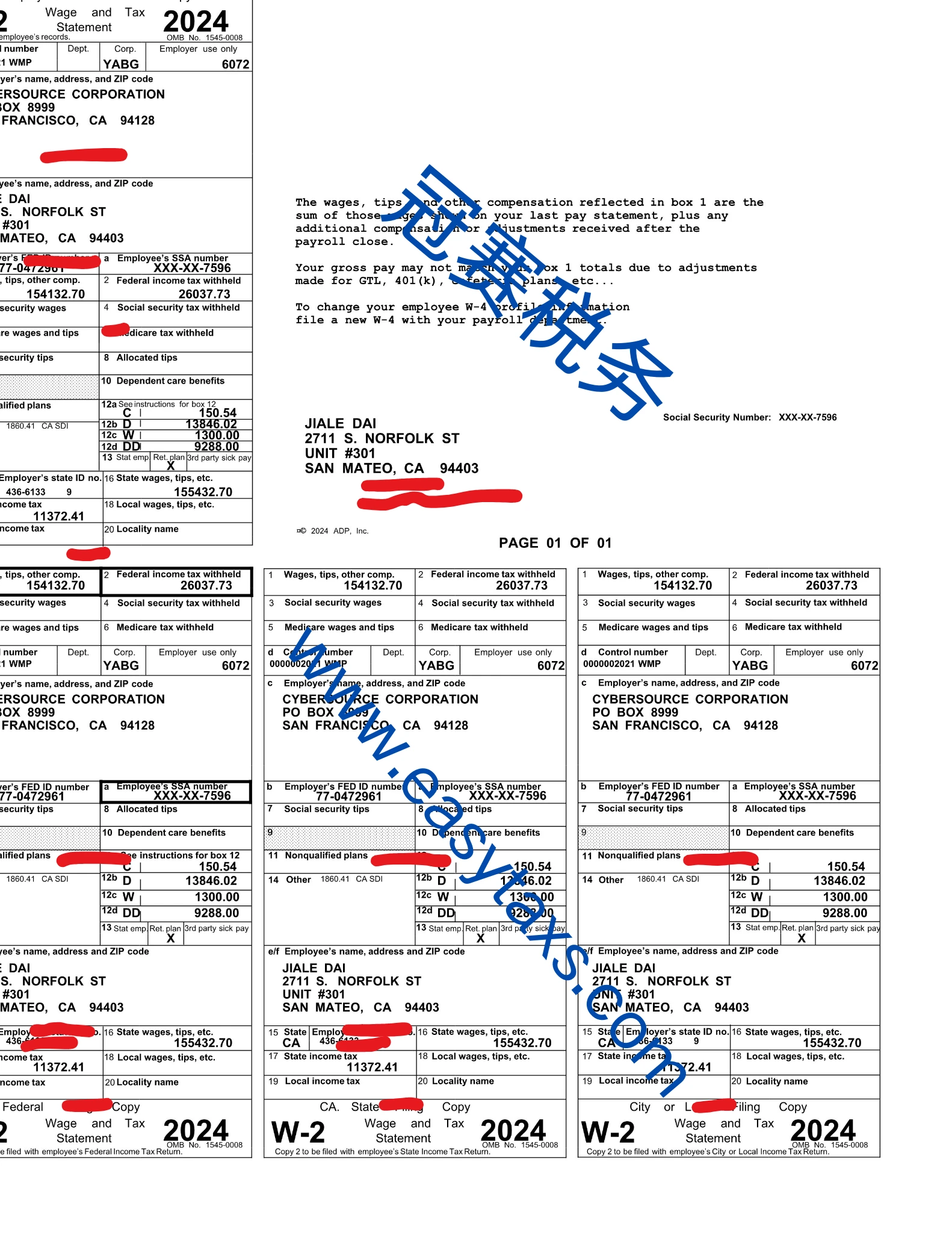

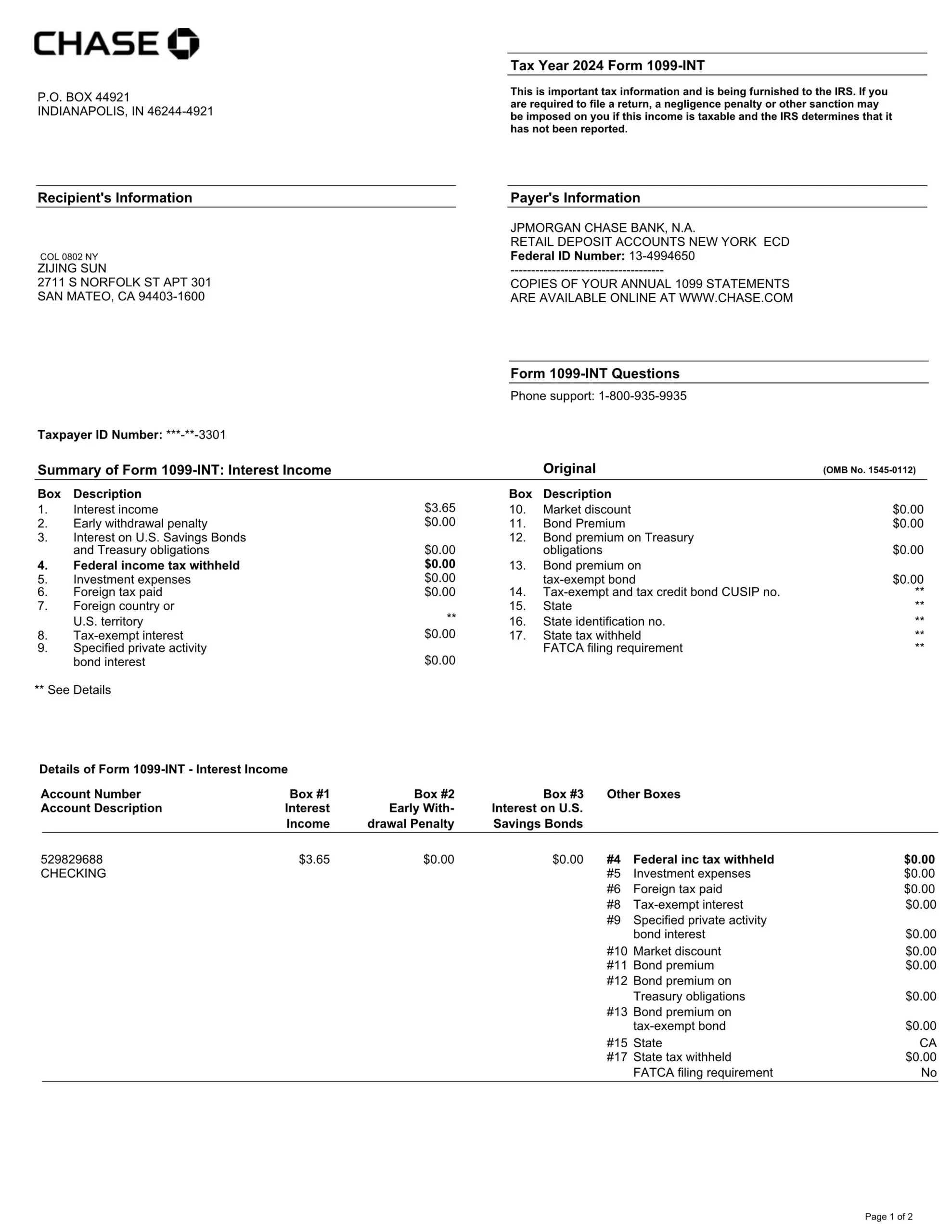

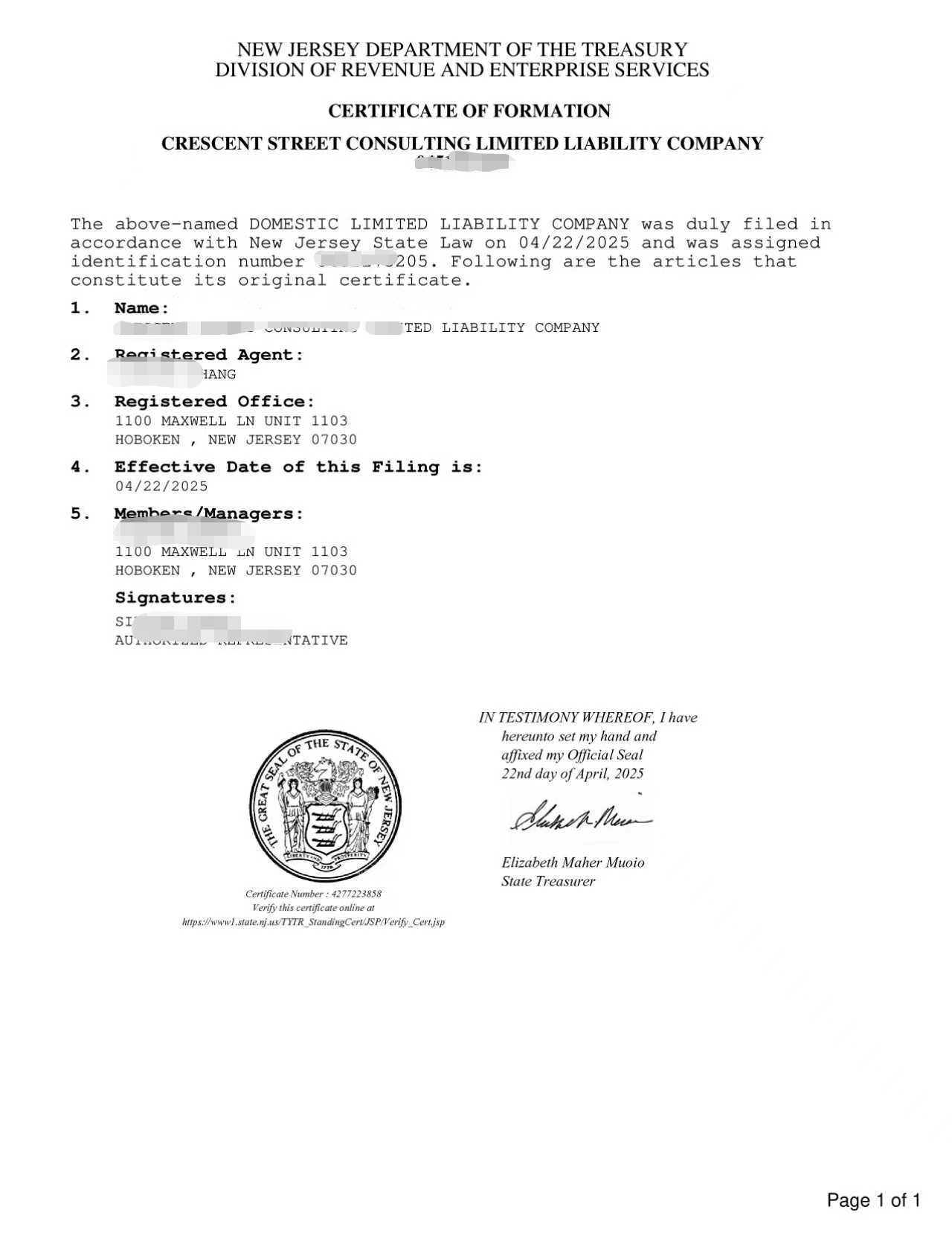

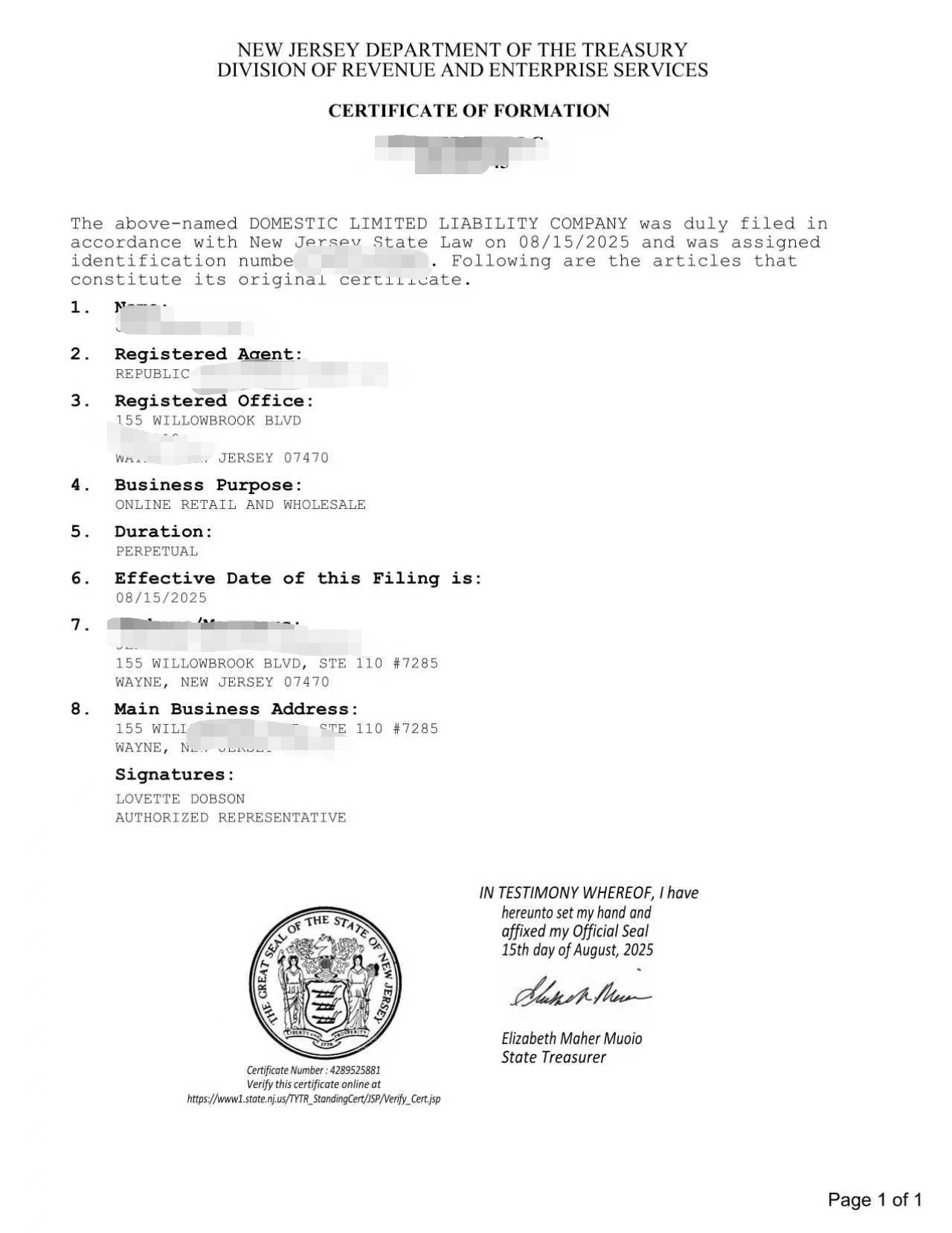

Business Registration Showcase

Why Choose Us?

✅ Bilingual U.S.-China Tax Team:CPAs familiar with U.S.-China tax laws, full Chinese support to avoid misunderstandings.

✅ Federal + All-State Filing:We handle federal and all 50 state taxes, including franchise, sales, and payroll tax.

✅ Zero Filing for No Income:New or inactive companies can file zero-income returns to stay compliant.

✅ Filing + Extension Support:Need more time? We help file Form 7004 to avoid late penalties.

✅ Dedicated Advisor Service:1-on-1 advisor ensures clear communication and progress tracking.

✅ Tax Amendment & Support:Filed incorrectly? We help amend returns (e.g., 1120X) to reduce risks.

What We Can Do for You?

Federal & State Tax Filing

Zero-Income Filings for Inactive Companies

Tax Extension Filing (Form 7004)

Late Filing & Penalty Resolution

Amended Returns (e.g., Form 1120X)

Franchise Tax Compliance

Sales Tax & Use Tax Filing

Payroll Tax Filing & W-2/1099 Reporting

Form 5471 5472 + 1120 for Foreign-Owned LLCs

ITIN-Related Tax Filing

Nexus & Multi-State Tax Issues

Registered Agent & Annual Report Management

IRS Audit Support

Entity Type Analysis & Conversion

Bookkeeping & Tax ReconciliationS-Corp Election (Form 2553)

Business Restructuring for Tax Efficiency

Estimated Tax Planning & Quarterly Payments

U.S. Corporate Tax Filing: Full Process & Steps

Step 1: Determine Entity Type & Required Tax Form

Different entities file different forms: C Corporation: Form 1120; S Corporation: Form 1120-S (must have filed Form 2553 election)

LLC:Single-member: Form 1040 Schedule C (or Form 1120 + 5472 for foreign-owned LLCs) ; Multi-member: Form 1065

Step 2: Prepare Financial Records

Gather all necessary records for the tax year, including: Income, expenses, cost of goods sold, and net profit;Bank statements, invoices, payroll, depreciation schedules;W-2s, W-3s, 1099-NEC, Forms 941 and 940 if applicable

Step 3: Complete the Tax Return

Fill out the appropriate tax form using the financial data;Calculate taxable income, deductions, credits, and final tax due;Apply available tax credits or carryforwards if eligible

Step 4: Apply for an Extension (if needed)

If more time is required, file Form 7004 for an automatic 6-month extension;Note: Extension applies to filing only, not tax payment—estimated taxes must still be paid by the original deadline

Step 5: Submit Your Return (e-file or mail)

Most corporations e-file directly to the IRS and relevant state agencies;Paper filing is also acceptable but less efficient;You may file on your own or authorize a tax preparer with a valid PTIN

Step 6: Pay Any Taxes Owed

Pay via IRS online system (irs.gov/payments), EFTPS, check, or credit card;Pay federal and state taxes separately as required

Step 7: Retain Filing Records

Keep a copy of the tax return, payment confirmations, and IRS acknowledgments;Recommend storing for at least 7 years in case of audit or correction

U.S. Company Annual Report / Annual Filing

Annual compliance (often called annual renewal or annual report filing) refers to the required filings and payments that a U.S. company must complete each year to stay in good standing with the state government.

📌 Key Components Include:

Annual Report Filing

Most states require companies to submit an annual or biennial report to update business information such as address, ownership, and registered agent.Franchise Tax Payment

Certain states (e.g., Delaware, California, Texas) require companies to pay a yearly franchise tax, even if the company has no income or activity.Registered Agent Fee

If your company uses a registered agent service, you must renew this service yearly.Business License Renewal (if applicable)

Some states or local jurisdictions require an annual renewal of business licenses or permits.

Frequently Asked Questions